Understanding Margin Trading Interest Rates: What Every Trader Needs to Know

Margin Trading Interest Calculator

Calculate Your Margin Interest

Enter your trading details to see how much interest you'll pay on your margin loan.

Interest Breakdown

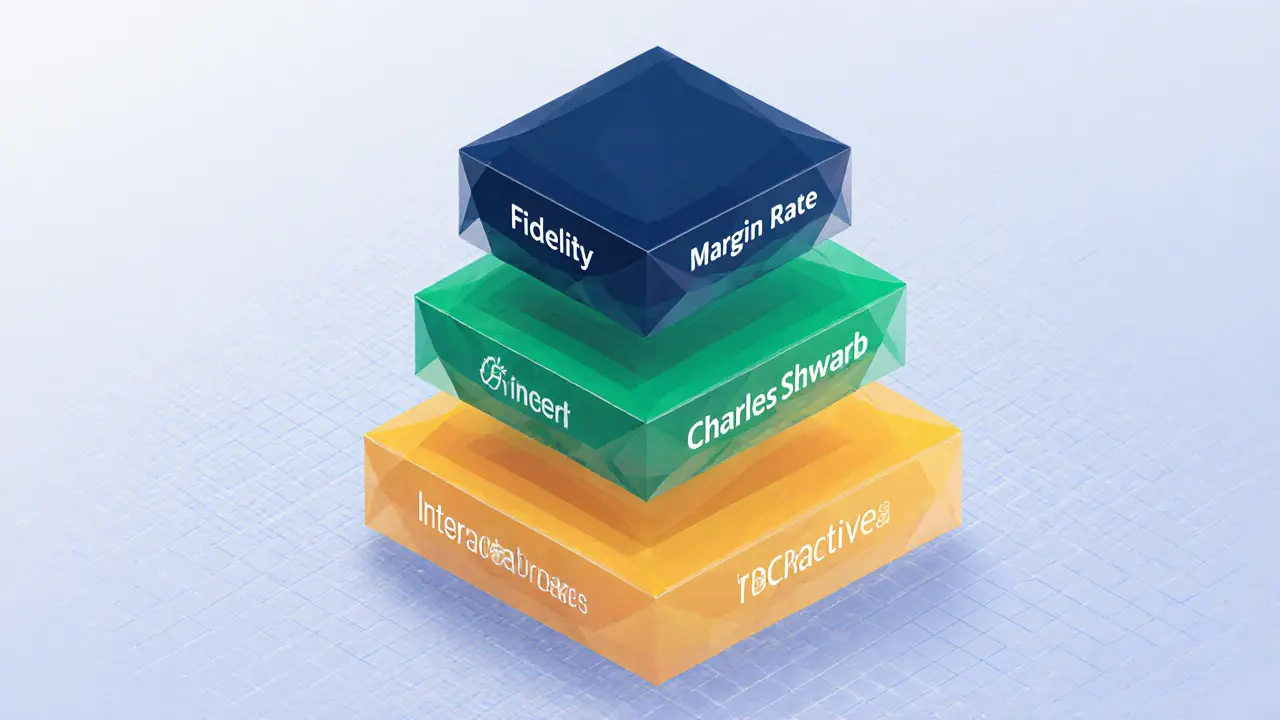

Current Margin Rate Comparison

Tiered rates from major U.S. brokers (as of September 2025):

| Broker | Balance Tier | Annual Rate |

|---|---|---|

| Fidelity Investments | Under $25,000 | 12.325% |

| Fidelity Investments | $25,000 - $999,999 | 10.575% - 8.00% |

| Charles Schwab | Under $25,000 | 12.325% |

| Charles Schwab | $250,000 - $499,999 | 10.575% |

| Interactive Brokers | Top tier (> $1M) | 4.339% |

When you hear the term Margin Trading Interest Rates is the cost you pay to borrow money from a broker so you can buy securities on margin, the first thought is usually “how much will it eat into my profits?” It’s a simple question with a surprisingly big impact on every leveraged trade you hold longer than a day.

Key Takeaways

- Margin rates today sit between 8.00% and 12.325% annualised, depending on the broker and loan size.

- Rates move in step with the Federal Reserve’s policy rate, usually 200‑400 basis points higher.

- Tiered pricing means larger loans cost less per dollar - a $1M loan can be half the rate of a $10K loan.

- Daily interest = (Borrowed Amount × Annual Rate ÷ 365) × Days held.

- Shop around - a 1% rate difference saves $365 per $100K borrowed each year.

How Brokers Set Their Rates

Each brokerage sets its own margin pricing, but three forces drive the numbers:

- Cost of capital - What the broker pays the Fed or other lenders.

- Risk premium - Compensation for the chance a trader can’t repay.

- Competitive pressure - Traders can easily compare rates online.

The Federal Reserve adjusts the federal funds rate, and brokers typically add 200‑400 basis points. That explains why today’s rates hover around 10% when the Fed’s target sits near 4.5%.

Current Tiered Rate Structures (September2025)

Below is a snapshot of three major U.S. brokers. All rates are annualised and apply to USD‑denominated margin loans. Tier thresholds are approximate; exact pricing may vary with account type or negotiation.

| Broker | Balance Tier | Annual Rate |

|---|---|---|

| Fidelity Investments | Under $25,000 | 12.325% |

| Fidelity Investments | $25,000 - $999,999 | 10.575% - 8.00% (rates fall as balance grows) |

| Charles Schwab | Under $25,000 | 12.325% |

| Charles Schwab | $250,000 - $499,999 | 10.575% |

| Interactive Brokers | Top tier (>$1M) | 4.339% (USD rates, exact figure varies by market) |

Calculating Your Daily Cost

The math is straightforward, but the impact compounds quickly:

(Borrowed Amount × Annual Rate ÷ 365) × Days held = Daily Interest

Examples:

- Borrow $10,000 at 10.825% → $10,000 × 0.10825 ÷ 365 ≈ $2.97 per day.

- Hold that position for 5 days → $2.97 × 5 ≈ $14.85 in interest.

- Borrow $100,000 at the same rate → $29.66 per day, $148.30 over a five‑day swing trade.

Day traders often avoid interest because most brokers waive it for positions closed within the same trading day. Swing traders and long‑term investors must budget margin interest as a fixed cost regardless of market moves.

Strategic Implications for Different Trading Styles

Day Trading: Interest is negligible if you close positions before the market settles. Focus instead on commission structures and capital efficiency.

Swing Trading (2‑10 days): Even a modest rate adds up. A 0.5% daily cost on a $50K margin loan equals $250 per week - a factor that can flip a marginally profitable trade into a loss.

Position Trading (weeks‑months): Margin interest becomes a major line item. Traders often limit leverage to 2‑3× and target stocks with high dividend yields to offset the cost.

Risk Management Tips Around Margin Costs

- Incorporate daily interest into your stop‑loss calculations.

- Use the tiered structure to your advantage - concentrate larger loans in a single broker that offers the best low‑rate tier.

- Monitor the Fed’s policy meetings; a 25‑basis‑point swing can shift your annual cost by $250 on a $100K loan.

- Set an “interest budget” - for example, no more than 2% of expected profit should go to margin interest.

Regulatory and Disclosure Landscape

Brokerages must disclose margin rates clearly in their agreements. The SEC requires that the interest be calculated daily and posted monthly. Failure to understand these disclosures can lead to surprise charges that erode capital.

Future Trends: Where Are Margin Rates Heading?

Two forces are shaping the next wave of margin pricing:

- Fintech competition - Zero‑commission platforms are experimenting with lower, usage‑based margin fees to attract retail clients.

- Personalized risk modeling - Advances in AI enable brokers to price loans based on individual credit profiles, not just balance tiers.

Analysts expect rates to stay within 200‑400 basis points of the Fed’s target, but the spread between the best and worst tiers could compress as new entrants drive price competition.

Final Checklist Before Opening a Margin Loan

- Know the broker’s tiered schedule and your projected balance.

- Calculate daily interest for your expected holding period.

- Align your trade’s expected return with the cost of borrowing.

- Monitor Federal Reserve announcements for rate shifts.

- Read the broker’s margin agreement for hidden fees (e.g., minimum interest charges).

Frequently Asked Questions

How often do brokers update margin interest rates?

Most major brokers review rates quarterly, but they may adjust immediately after a Fed policy change. Retail clients usually receive an email or portal notice before the new rates take effect.

Can I negotiate a lower margin rate?

Yes, especially if you hold a substantial balance or have a longstanding relationship with the brokerage. Interactive Brokers, for instance, offers custom pricing for accounts over $1M.

What happens if I forget to close a margin position before the month ends?

Interest accrues daily and is posted to your account at month‑end. If the balance plus accrued interest falls below the maintenance requirement, the broker can issue a margin call or liquidate positions.

Do margin interest rates differ for non‑USD accounts?

Yes. Brokers often apply a spread to the local overnight funding rate for each currency. For example, EUR‑based margin loans might sit 0.5‑1.0% higher than the USD tier due to Euro‑zone funding costs.

Is margin interest tax‑deductible?

In the United States, margin interest is generally deductible as investment interest expense, subject to limits based on your net investment income. Consult a tax professional for specifics.

9 Comments

Jessica Smith

October 3, 2025 at 21:08

Anyone who uses margin without calculating daily interest is just gambling with someone else’s money. I’ve seen people blow up accounts because they thought ‘it’s just a few bucks’ - until they woke up to a $2K interest bill for a $50K loan. Wake up. This isn’t fantasy football.

Petrina Baldwin

October 4, 2025 at 11:34

Brokers hide this stuff in fine print. Always check the agreement.

Ralph Nicolay

October 4, 2025 at 21:43

It is imperative to note that the Federal Reserve's policy rate serves as the foundational benchmark upon which brokerage firms establish their margin interest rates. Failure to account for this relationship may result in significant miscalculations regarding the true cost of leverage.

sundar M

October 5, 2025 at 11:54

Yo this is actually super useful! I was just using Fidelity without realizing how much I was paying on my $80K loan. Just switched half to Interactive Brokers after seeing that 4.3% tier - saved me like $500/month. Brokers are so greedy, but you can beat them if you know the game. Thanks for the breakdown 🙌

Nick Carey

October 6, 2025 at 10:08

Ugh I hate math. Can’t we just get a flat rate like Netflix?

Sonu Singh

October 6, 2025 at 17:52

Great post! But typo in table - Schwab tier says $250k-$499k at 10.575% but should be $100k-$249k for that rate. Also, don't forget tax deductibility - I claimed $1.2k last year as investment interest. Talk to your CPA!

Peter Schwalm

October 6, 2025 at 18:11

One thing people miss: if you’re swing trading, treat margin interest like rent. You wouldn’t rent a house without knowing the monthly cost - why treat your trades differently? Build the interest into your profit target before you even open the position. It’s not a surprise cost, it’s a fixed expense. Plan for it.

Alex Horville

October 6, 2025 at 23:42

Why do American brokers charge 12% when Europe charges 3%? It’s because the Fed is corrupt and Wall Street rigs the system. We need to stop letting banks bleed retail traders dry. This isn’t capitalism - it’s exploitation.

Marianne Sivertsen

October 7, 2025 at 05:51

There’s something quiet about margin interest - it doesn’t scream like a loss, but it bleeds you slowly. I used to think I was winning until I added up six months of it. Now I only use margin if the trade can cover the interest and still double my money. It’s not about being right - it’s about being patient enough to wait for the right bet.